A major new tax change is already impacting your member communications and year-end reporting workflows: borrowers may be able to deduct qualified vehicle loan interest, and lenders now have new IRS information reporting responsibilities tied to that deduction.

If you’re a credit union, this is about more than compliance. It’s a member experience moment—because the first place members will call when they hear “car loan interest is deductible” is your contact center.

Here’s a practical guide to what’s required for calendar year 2025 interest, what we know about the new reporting form, and how to get your systems ready.

The big picture: why lenders are now involved

For tax years 2025 through 2028, individuals may be able to deduct interest paid on a qualifying passenger vehicle loan (subject to eligibility and income phase-outs). Because the deduction exists, Congress created a corresponding lender reporting regime—similar in concept to mortgage interest reporting.

The key lender takeaway: if you receive $600+ of interest from an individual on a covered auto loan in a calendar year, the loan can trigger reporting obligations.

Step 1: Know what loans are in-scope (so you don’t over- or under-report)

A “specified passenger vehicle loan” generally means: a loan originated after 12/31/2024, used to purchase a qualifying passenger vehicle for personal use, and secured by a first lien on that vehicle. Certain categories are excluded (for example: fleet, commercial-only use, leases, salvage/scrap situations).

Quick “in-scope” checklist for lenders

- Flag loans that are:

- Consumer/personal-use vehicle loans (not business-use only)

- Secured by a first lien on the vehicle

- Originated after 12/31/2024

- Connected to a vehicle that meets the program requirements (new purchase + final assembly in the U.S., under 14,000 lbs GVWR)

Even if you aren’t validating every consumer’s tax eligibility, you do want to cleanly identify the population most likely to request a statement and most likely to be required in future years.

Step 2: What you must deliver for 2025 interest (transition relief)

Here’s the good news for lenders: the Treasury/IRS issued transition relief for calendar year 2025.

For 2025 only, you can satisfy the new 6050AA reporting obligation by:

Making a statement available to the borrower on or before January 31, 2026 showing the total amount of interest received in calendar year 2025 on the specified passenger vehicle loan.

This can be delivered via:

- Online account portal (easy member access)

- Regular monthly statement

- Annual statement

- Other similar means designed to provide accurate info

This transition approach exists because the IRS and lenders need time for systems and form programming updates—and the IRS indicated it will not impose certain information reporting penalties if you follow the transition method for 2025.

Practical guidance: what your 2025 “recipient copy” should look like

For 2025, think of this as a Year-End Vehicle Loan Interest Summary rather than a brand-new IRS form. Minimum viable content:

- Member/borrower name

- Loan/account identifier (masked)

- Calendar year (2025)

- Total interest received in 2025

- Lender contact info for questions

Recommended add-ons (to reduce calls and prep you for 2026+):

- Vehicle year/make/model + VIN (or last 6 of VIN)

- Loan origination date

- “First lien” indicator (internal)

- Short disclaimer that eligibility/deductibility depends on IRS rules

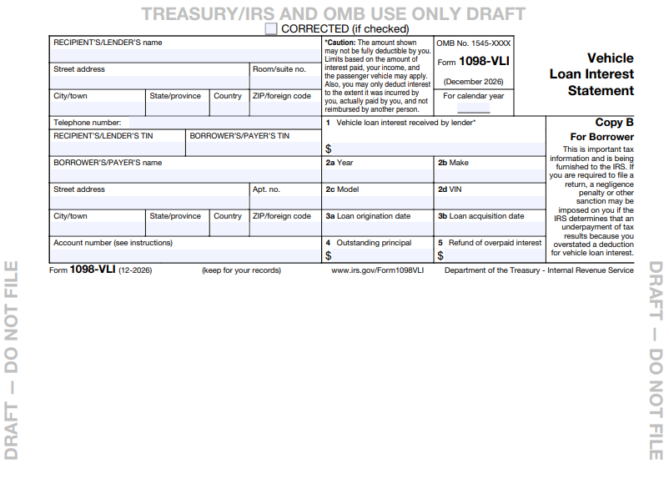

Step 3: What’s likely coming next: Form 1098-VLI and “full” reporting

The IRS has released a draft of a new form called Form 1098-VLI (Vehicle Loan Interest Statement). Drafts can change, but it provides a strong preview of the data fields lenders should be prepared to produce.

The draft form reflects fields such as:

- Vehicle loan interest received by lender

- Vehicle year / make / model / VIN

- Loan origination date

- Loan acquisition date (important for indirect lending, loan purchases, and mergers)

- Outstanding principal (snapshot as of Jan 1 of the reporting year, with special handling if originated/acquired during the year)

- Refund of overpaid interest (if applicable)

Separate from the form, the statute describes required data elements for the information return, including borrower name/address, total interest, principal at the beginning of the year, origination date, and vehicle identifiers.

Bottom line: even if 2025 is “statement-only,” you should use 2025 to build the data pipeline you’ll need when “full reporting” becomes required.

Step 4: A lender implementation checklist (designed for credit unions)

A. Data readiness (core + collateral + LOS)

Make sure you can reliably produce:

- Borrower name/address (as of year-end)

- Borrower TIN handling (where appropriate in future form workflows)

- Interest received by calendar year (not just paid-to-date)

- Principal balance snapshot as of January 1

- Loan origination date

- Vehicle year/make/model and VIN (and validation rules)

- Loan acquisition date (if your CU acquires loans)

Tip: Build exception reporting for missing VINs or incomplete collateral records now—before January.

B. Member experience + contact center readiness

Prepare scripts for the inevitable questions:

- “Do I qualify for the deduction?”

- “Why doesn’t my loan qualify?” (lease, used vehicle, non-U.S. final assembly, business use, etc.)

- “Is the entire amount deductible?” (often no—income phaseouts and other limits apply)

- “Where do I enter the VIN?” (tax software/return requirement)

C. Delivery method (portal vs paper)

- Decide how you’ll deliver the 2025 statement:

- Portal-first (fast + searchable + reduces cost)

- Paper for members who opted out of e-delivery

- Hybrid, with a consistent subject line and downloadable PDF

D. Compliance calendar

- Now → Jan 2026: identify in-scope loans; produce total interest for 2025; publish/send statement

- By Jan 31, 2026: member statement available

- During 2026: implement full 1098-VLI style reporting capability (data + print/mail/e-delivery + e-file workflows)

- Future year operations will likely follow standard information return timing (recipient statements first, then IRS filing deadlines)

Sample copy: “2025 Vehicle Loan Interest Summary” (portal / PDF / annual statement)

Subject: 2025 Vehicle Loan Interest Summary (for tax reporting)

Hello [Member Name],

This statement shows the total vehicle loan interest received in calendar year 2025 for the loan below:

- Loan/Account: XXXX1234

- Tax Year: 2025

- Total Interest Received in 2025: $X,XXX.XX

If you have questions about this statement, contact:

[Credit Union Name] | [Phone] | [Address] | [Hours/Support URL]

Important: Tax deductibility depends on IRS rules and your individual circumstances. This statement reports interest received by the lender for the year.

The “why now” message you can share internally

If you’re prioritizing projects for Q1: this one matters because it touches core servicing, data quality, member communications, and potentially high-volume annual statement delivery.

Treat 2025 as your “soft launch” year:

- Deliver the required 2025 total-interest statement cleanly

- Build the collateral/interest/principal snapshot pipeline

- Be ready if/when Form 1098-VLI becomes the standard for upcoming years

How EOS can help

EOS works with financial institutions to support compliant, secure delivery of year-end statements and regulatory communications — across print, digital, and hybrid workflows. Whether you’re preparing a one-time 2025 interest summary or planning for future Form 1098-VLI reporting, having a reliable statement delivery process in place can simplify compliance and improve the member experience.